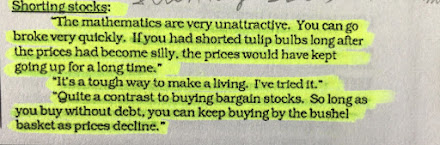

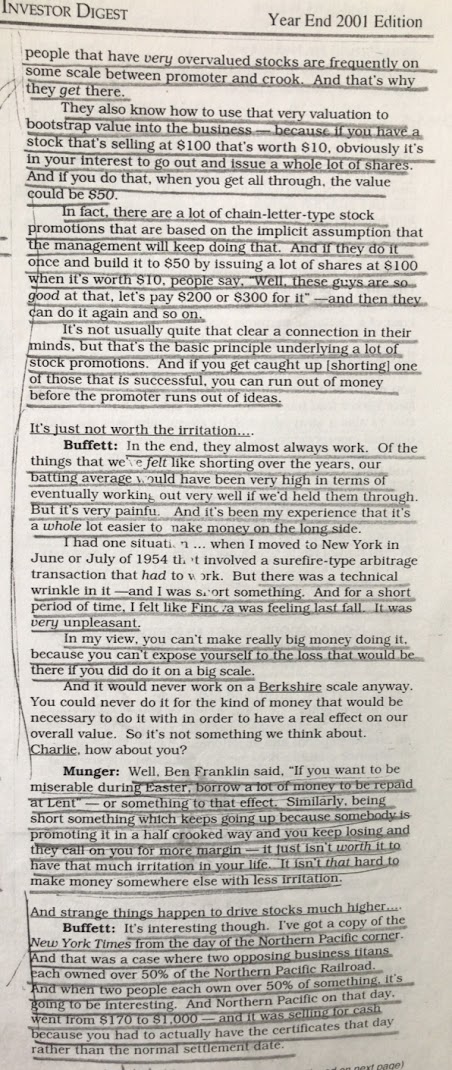

What should one do when the facts change and the original thought process doesn't hold any longer. As an investment professional, situations that warrant a change of mind come with a little higher frequency. New facts emerge and decisions have to be constantly revisited in light of those. In this post, I have listed down a few quotes that I remember and questions that I ask which help me decide. It's possible that you too may find them useful in your decisions, investments or otherwise.

When the facts change, I change my mind. What do you do, Sir ?

This quote from Keynes has been my guiding light when I have to make decisions in the light of new facts.

The other person's viewpoint seems more rational and logical than mine. How should I handle my ego which prevents me from accepting it?

Focus on what is right, not who is right. If my existing point of view is inferior to an alternate view point, I should immediately latch on to the better one. Knowledge like sunshine should be welcomed from all directions. It doesn't matter who the person on the other side is. Focus only on what is right.

How long will this change be required ?

Till my last breath. Munger of his own admitting made the worst investment mistake by investing in Alibaba during the last few years of his life. But when he realised he was wrong, he quickly sold his investment and didn't fall for commitment. Even in his last years, he taught an important lesson through his actions. If you realise you are wrong, change the course. Period.

What is my North Star while investing ?

I consider the investment thesis (moat around the business, its sustainability, the track record in terms of return on capital, risks and the quality of management) as the North Star. In a plethora of decision making points, I look upto my North Star. If the investment thesis continues to be as I thought earlier, no change is required even if the market doesn't agree with me for years together. I tell myself that I should be patient, stay put and not disturb the position.

What should an ideal mind be like ?

An ideal mind should be like a spider's web. As soft as silk but stronger than steel. When conditions warrant, the mind should change itself effortlessly. However, when nothing has changed, it should be as hard as steel. Unmoved and firm. Like Angad's leg.

Should you change your mind about an investment idea, what about loss of face in front of the clients?

It's better to look foolish than to stay foolish.